what is excellent credit according to usda rural loans

USDA abode loans offer 100% financing, low rates, and affordable payments. These loans are becoming more pop past the day, as buyers observe an easier way to buy a habitation with zero down payment.

There are iii types of USDA dwelling house loans:

Loan guarantees:The USDA guarantees a loan issued by a local lender, assuasive borrowers to benefit from low mortgage involvement rates and a low down payment.

Direct loans:These mortgages for low-income applicants are issued by the USDA, with interest rates every bit depression as 1%.

Habitation improvement loans and grants:These loans are intended to help homeowners repair or upgrade their homes, up to $27,500.

Click hither to verify your USDA abode loan eligibility in minutes (Apr 7th, 2022)

In this article:

- USDA-eligible geographic areas

- Advantages of USDA habitation loans

- USDA loan income limits

- USDA loan mortgage rates

- Credit score minimums

- USDA loan FAQ

- Our recommended USDA lenders

What is the USDA loan programme?

The U.s.a. Department of Agriculture (USDA) sets lending guidelines for the program, which is why it is also called the USDA Rural Development (RD) Loan. This mortgage type reduces costs for homebuyers in eligible rural and suburban areas. Information technology is one of the most cost-effective abode buying programs in the marketplace today.

Since its inception in 1949, the USDA Rural Development loan has helped over 1 million home buyers obtain housing with trivial or no money downwards.

Who is eligible for a USDA home loan?

The USDA dwelling house loan is available to borrowers who see income and credit eligibility requirements. Qualification is easier than for many other loan types, since the loan doesn't crave a down payment or a high credit score. Homebuyers should make sure they are looking at homes within USDA-eligible geographic areas, because the property location is the almost important gene for this loan type.

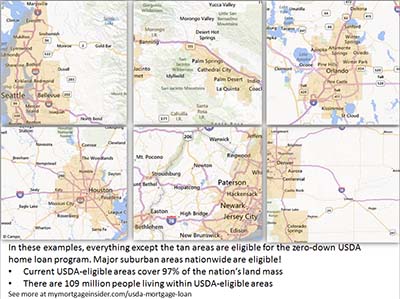

USDA Mortgage Eligible Geographic Areas

The property must be located in a USDA-eligible area. Borrowers tin can search USDA'south maps to browse certain areas or pinpoint a specific accost. If you lot are unsure if a property is eligible, check with a USDA loan officer here (Apr 7th, 2022)

Remember your area is not eligible? Well, nigh 97% of U.s. land mass is USDA-eligible, representing 109 million people. Many properties in suburban areas may be eligible for USDA financing. It's worth checking, even if yous think your expanse is too developed to exist considered "rural". The USDA eligibility maps are still based on population statistics from the demography in the year 2000. This is a unique opportunity to finance a suburban dwelling house with this nada-down mortgage program before the USDA updates their maps.

Evidence me today'southward USDA rates (April 7th, 2022)

Upcoming Eligible USDA Map Changes

USDA had slated changes to its eligibility maps for October 1, 2015. Nonetheless, according to a source within USDA, map changes had been postponed.

Co-ordinate to the source, eligibility maps are now reviewed every iii to five years. The last review happened in 2014.

USDA runs on a fiscal year of October 1 through September 30. This is why most big changes to the program happen in Oct. For this reason, watch for a geographical purlieus change on October 1, 2020.

Changes are more likely in 2020 and 2021. The reason: The 2020 demography. USDA bases its maps on these United states of america-broad population counts that happen every ten years. Since the USDA has not made major changes to maps since the year 2000, it'due south condign more and more probable that big updates volition happen presently.

Advantages of USDA Domicile Loans

Zero Downward (100% Financing)

Easily down, the about important characteristic of the USDA loan is that it requires zero down. It allows for 100% financing of an eligible home'south purchase price. FHA loans require a minimum of 3.five% downwardly payment, adding thousands to upfront expenses. The no-coin-down feature has allowed many people to buy a home who would otherwise be locked out of homeownership.

Hither's your take a chance at a nix-down home loan. Employ here (Apr 7th, 2022)

The USDA Guarantee

The USDA loan is guaranteed by the U.Due south. government — specifically by the U.S. Department of Agriculture. Guaranteed does non mean that every borrower'south blessing is certain. Rather, it means that USDA will reimburse lenders if the borrower defaults on the loan. The USDA backing removes much of the run a risk from the loan and allows banks and mortgage companies to offer a cipher-down loan at incredibly low rates.

The USDA Guarantee Fee

The lender guarantee is partially funded by the USDA mortgage insurance premium, which is one.00% of the loan amount (decreased from 2.75% on October 1, 2016). The loan likewise has a 0.35% annual fee (decreased from 0.fifty% on October 1, 2016).

The almanac fee is paid monthly in twelve equal installments. For each $100,000 borrowed, the upfront fee is $one,000 and the monthly premium is $29.

The borrower tin coil the upfront fee into the loan amount or pay information technology out-of-pocket. Compared to other loan types like FHA, or the private mortgage insurance (PMI) on conventional loans, the USDA mortgage insurance fees are among the lowest.

USDA Loans Have Been Cheaper Since 2016

On Oct i, 2016, USDA reduced its monthly fee from 0.50% to 0.35%. Your monthly cost equals your loan amount or remaining principal remainder, multiplied by 0.35%, divided by 12.

Additionally, the upfront fee fell from ii.75% to just ane.00%. This is a good opportunity for home buyers to get lower monthly payments with this loan plan.

USDA Domicile Loan Income Limits

Guaranteed loans are available to "moderate" income earners, which the USDA defines as those earning upwards to 115% of the area'south median income. For instance, a family of four buying a property in Calaveras County, California tin earn upwards to $92,450 per year.

The income limits are generous. Typically, moderate earners find they are well inside limits for the program.

It's also important to keep in mind that USDA takes into consideration all the income of the household. For instance, if a family with a 17-twelvemonth-old child who has a job will have to disclose the kid'southward income for USDA eligibility purposes. The child'south income does not need to exist on the loan awarding or used for qualification. But the lender volition look at all household income when determining eligibility.

Click here to verify your USDA home loan eligibility (Apr seventh, 2022)

USDA Loan Length

The USDA loan offers just two mortgage choices: 15- and 30-year fixed rate loans. These are the safest and most proven loan programs. Adjustable-rate loans are not available.

The USDA loan offers just two mortgage choices: 15- and 30-year fixed rate loans. These are the safest and most proven loan programs. Adjustable-rate loans are not available.

Low USDA Mortgage Rates

Private banks and mortgage companies offering USDA loans at very low rates. The USDA backs these loans, making information technology safer and cheaper for private banks and mortgage companies to lend. The savings are passed on to the home heir-apparent in the grade of lower rates.

USDA loan rates are often lower than those available for conventional and FHA loans. Home buyers who choose USDA frequently end up with lower monthly payments considering higher mortgage insurance fees associated with other loan types.

Show me today's USDA mortgage rates (Apr 7th, 2022)

Closing Cost Options

USDA loans let the seller to pay for the buyer's closing costs, upward to three% of the sales price. Borrowers can besides use gift funds from family members or qualifying non-turn a profit agencies to kickoff endmost costs when they supply this downloadable USDA souvenir letter signed past the donor.

USDA loans as well permit borrowers to open up a loan for the full corporeality of the appraised value, even if it's more than the purchase price. Borrowers can utilize the excess funds for closing costs. For example, a habitation's price is $100,000 just it appraises for $105,000. The borrower could open a loan for $105,000 and use the actress funds to finance closing costs.

Asset Requirements

Borrowers who don't accept all their closing costs paid for by the seller or otherwise need cash to shut the loan will demand to prove they accept adequate assets. Two months banking concern statements will exist required.

There's also a requirement that the borrower must non accept plenty assets to put 20% downward on a home. A borrower with plenty avails to qualify for a conventional loan will not authorize for a USDA loan.

Debt Ratios – 2020 To Maintain Changes Rolled Out In 2014

The programme adopted new debt ratio requirements on December 1, 2014. There are no planned updates to this policy in 2020.

Prior to December 2014, there were no maximum ratios as long as the USDA computerized underwriting system, called "GUS", approved the loan. Going forward, the borrower must have ratios beneath 29 and 41. That means the borrower'southward business firm payment, taxes, insurance, and HOA dues cannot exceed 29 percentage of his or her gross income. In addition, all the borrower'south debt payments (credit cards, car payments, student loan payments, etc) added to the total house payment must be below 41 percentage of gross monthly income.

For example, a borrower with $4,000 per month in gross income could accept a house payment as high as $ane,160 and debt payments of $480.

USDA lenders can override these ratio requirements with a transmission underwrite – when a person reviews the file instead of the algorithm. Borrowers with great credit, spare coin in the banking company after endmost, or other compensating factors may be approved with ratios higher than 29/41.

Click here to check USDA rates (Apr 7th, 2022)

Credit Score Minimums – Updated for 2022

New credit score minimums went into upshot in 2014 and these will be carried over into 2022. Before the change, USDA loans could be approved with scores of 620 or even lower.

Every bit of December 1, 2014, USDA set a new credit score minimum of 640. This is not really a big change, since almost USDA lenders required a 640 score prior to the official USDA updates.

I of the Last Remaining 100% Financing Options

No money down loans appeared to have vanished during the housing bosom, but USDA loans remained bachelor throughout that time and are still available today. The growing popularity of the USDA loan has proven that zero-downwards loans are still in high demand.

Borrowers in designated rural areas should consider themselves lucky to have access to this low-cost, zero down loan option. Anyone looking for a domicile in a small town, suburban or rural area should contact a USDA loan professional to encounter whether they qualify for this great program.

USDA Home Loans FAQ

I'g looking to buy a home in a suburban area. Should I all the same look into USDA financing?

Yes. Many suburban areas across the country are eligible for a USDA loan. Complete a curt online questionnaire to find out if your area is eligible.

I thought USDA home loans were only for farms.

On the contrary, a USDA loan cannot be used to finance the purchase of an income-producing farm. In fact, homes with low acreage may be more than suitable for the program, since USDA may non allow a domicile if its land value is more than than 30% of the total value of the home. From the USDA handbook:

"Mostly, the value of the site must not exceed 30 percentage of the total value of the belongings. When the value of the site is typical for the area, as evidenced by the appraisal, and the site cannot be subdivided into two or more than sites, the 30 percent limitation may be exceeded."

Are USDA Loans Some Obscure Loan Type That No One Actually Uses?

No. Thousands of domicile buyers utilise USDA financing each year. These mortgage loans are getting more than popular all the time. Beneath is a map of how many loans were completed by country in 2015.

Data: CFPB

Does USDA offer a streamline refinance program?

Yes. To qualify, the borrower must currently have a USDA loan currently and must live in the habitation. The new loan is subject to the standard funding fee and annual fee, just like purchase loans. Refinancing borrowers must qualify using current income but may qualify with higher ratios than generally accepted if the payment is dropping and they accept fabricated their current mortgage payments on time.

If the new funding fee is not being financed into the loan, the lender may not require a new appraisal.

Can I get a structure loan with USDA?

Homebuyers who wish to build a habitation with a USDA loan can do so using the USDA construction loan program which combines a structure loan and a traditional 30-year fixed USDA loan into a single-close loan.

Can I buy a new construction dwelling house with a USDA mortgage?

Yes. In fact, a new domicile should meet USDA minimum standards even more easily than will an existing home. Many housing developments are going up in USDA-eligible areas, making this loan a great selection for new homes.

Utilize for a new construction USDA loan here (Apr seventh, 2022)

Does USDA require the property to be in skillful condition?

By and large, yep. The appraiser will country in the appraisement report whether or not the belongings conforms to minimum standards, which are the aforementioned property requirements needed for an FHA loan. Make sure your lender selects an FHA-canonical appraiser who can verify the property meets FHA standards.

Can I buy a vacation home with a USDA loan?

USDA loans are intended for the buy of primary residence. This type of housing loan cannot be used to purchase a second home.

Can I buy a condo or townhome with a USDA loan?

Yes, however, the lender has to confirm that the condo or townhome meets FHA, Fannie Mae, Freddie Mac or VA requirements. The lender assumes a lot of liability past certifying that a condo project meets these requirements, so they may not exist willing to approve USDA loan for a condo or townhome.

Tin I buy a manufactured home with a USDA loan?

USDA typically allows buyers to buy new manufactured homes just. While pre-existing manufactured homes are typically not allowed, they may exist adequate if the current possessor has a USDA domicile loan on the property. Ask your existent estate amanuensis for this data.

New manufactured homes must come across certain thermal performance standards and be permanently affixed to a foundation. It also must have a minimum living infinite of 400 square feet. A heir-apparent who is interested in a manufactured/mobile home should check with their real estate agent and lender about whether the home is USDA-eligible.

Are USDA dwelling house loans only for starting time-time homebuyers?

No. Buyers who have purchased before may utilise the USDA program. However, borrowers ordinarily have to sell their current home or show information technology's either too far away from their piece of work or otherwise is no longer suitable.

Click hither to verify your zero-down mortgage eligibility (Apr seventh, 2022)

Does USDA allow gifts to help with closing costs?

Yes. Gifts can be used provided they are from a relative, charitable organization, government entity, or nonprofit. In some cases, a gift from a friend tin can be used if proof of the relationship prior to the loan transaction tin can be established. Applicants receiving a gift will need to complete USDA'due south gift letter class. Download the form here.

What'south the minimum credit score allowed for a USDA loan?

USDA grants the highest approval levels to those with a 660 score and above. On December ane, 2014, USDA set a minimum score for the programme at 640. This was non a large change since most canonical lenders had already prepare their own minimum score at the same level.

I have no credit. Can I get a USDA loan?

Borrowers who don't have an established credit history may be able to qualify for a USDA loan. At least four non-traditional sources will be needed, such as:

- Rental history

- Utility payment records

- Insurance payments

Can I finance my funding fee even though my LTV will be more than 100%?

USDA does not consider the funding fee every bit part of its loan-to-value (LTV). And then in essence, USDA allows for an LTV of a piffling over 101%.

Why doesn't every buyer utilise the USDA home loan program?

Most homebuyers would adopt to do a USDA loan, but perhaps the areas in which they are looking are not USDA-eligible. Larger urban and surrounding areas are not eligible, since the betoken of the program is to encourage rural development. Nevertheless, a surprising number of adult suburban areas are however eligible.

Apply for USDA here

USDA home loan rates are low and gratuitous quotes are bachelor now. Check your eligibility for this programme and find out almost USDA-eligible areas near you. Complete a brusque online asking class to get started.

Click hither to verify your USDA eligibility (April 7th, 2022)

*Statistic per AskUSDA web log as of 2/28/2013.

Source: https://mymortgageinsider.com/usda-mortgage-loan/

0 Response to "what is excellent credit according to usda rural loans"

Postar um comentário